Table of Contents

- The money has already moved (and the bubble keeps not bursting)

- Adoption has already crossed the critical threshold

- On the workforce: the numbers that can’t be ignored

- The competitive landscape among models has shifted

- Agents are advancing, security is holding back the leap

- Two structural vulnerabilities worth bringing to the boardroom

- The governance picture

Here we go again, it’s that time of year. Stanford HAI has published the 2026 edition of its AI Index Report, and as every year, we’ve worked through it to pull out the most interesting insights.

It’s the document that more than any other captures the real state of artificial intelligence in the world — investments, adoption, workforce impacts, systemic risks. We read through the 400+ pages to extract what we consider the most relevant implications for executives and business leaders.

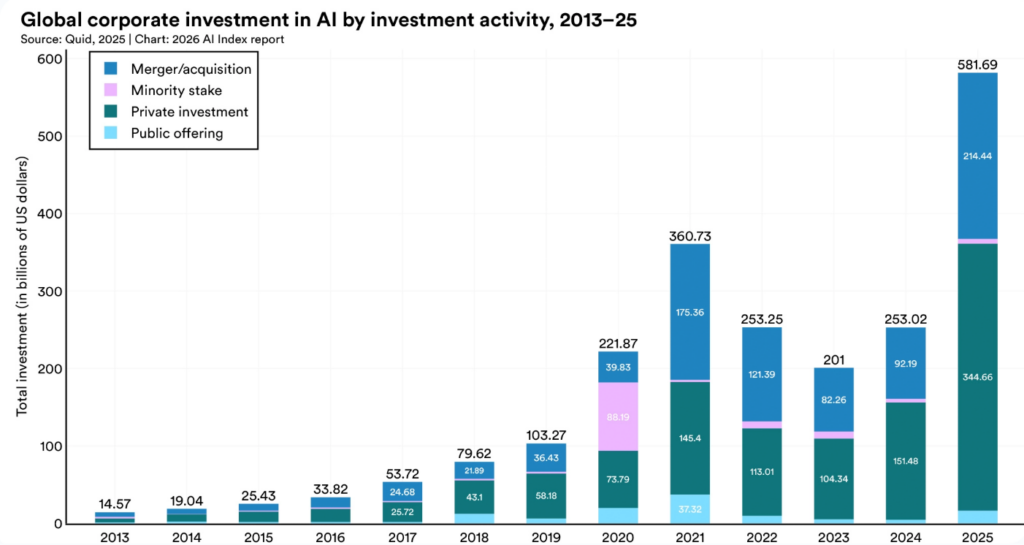

The money has already moved (and the bubble keeps not bursting)

Global private AI investment grew 127.5% in 2025. The United States invested $285.9 billion — roughly 23 times China’s $12.4 billion. The major hyperscalers (Amazon, Google, Microsoft, Meta, Oracle) have doubled infrastructure spending since the launch of ChatGPT. Google alone reported over $150 billion in capex in 2025.

The speed at which leading AI companies are reaching meaningful revenue exceeds that of any previous technology generation — including Uber and Moderna during their most aggressive growth phases.

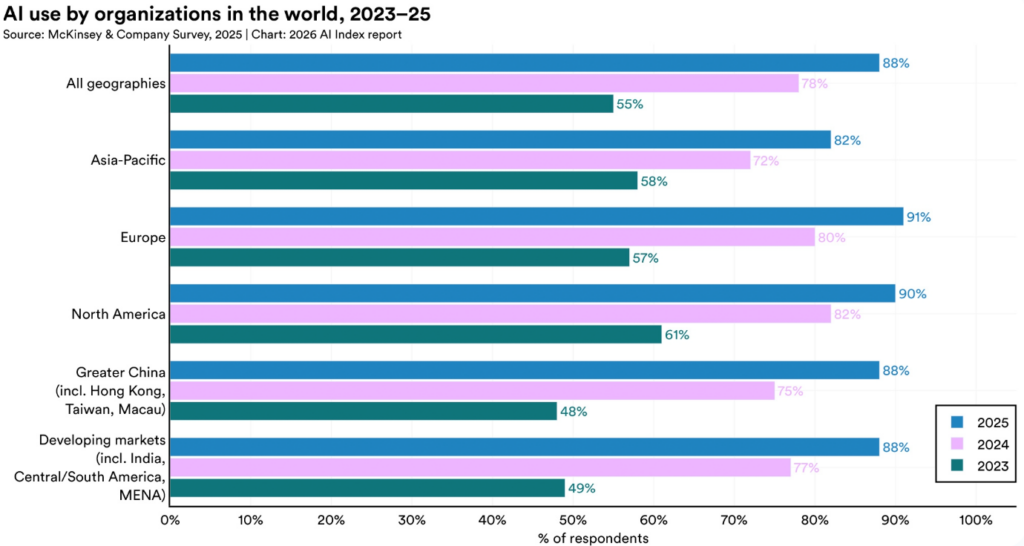

Adoption has already crossed the critical threshold

88% of organizations have adopted AI in some form. 70% regularly use generative AI in at least one business function. The value generated for American consumers reached $172 billion annually, with the median value per user tripling in a single year.

The share of organizations that have achieved full integration at scale remains in the single digits across nearly all business functions. Adoption is widespread; operational maturity is still rare.

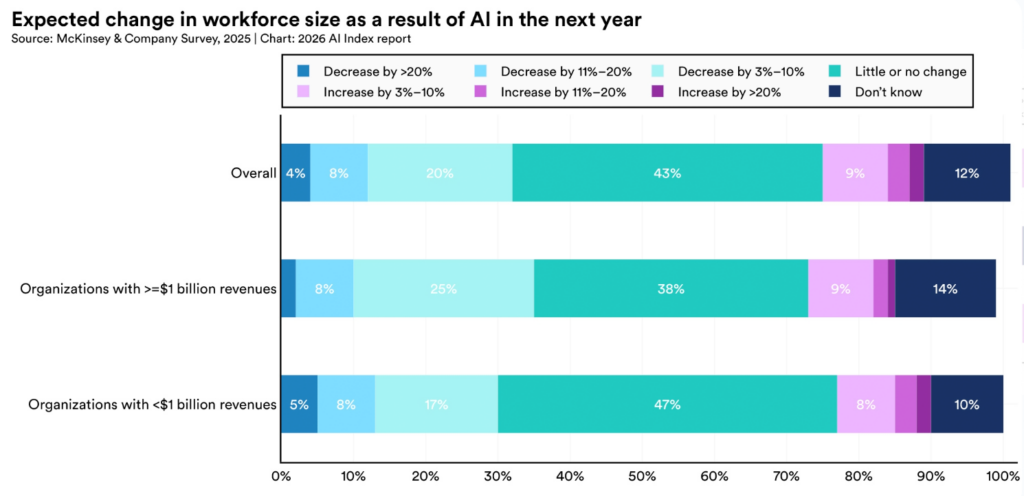

On the workforce: the numbers that can’t be ignored

Productivity gains are documented and real: +14–26% in customer support and software development. At the same time, entry-level roles in those same sectors are declining. US software developers aged 22–25 fell by nearly 20% from 2024. One third of organizations expect workforce reductions in the coming year, particularly in operations, supply chain, and software engineering.

There’s a less visible risk worth monitoring: the “learning penalty.” Junior professionals who rely heavily on AI develop technical skills more slowly. In the short term, they produce more; in the medium term they risk structural skill gaps. It’s a talent pipeline problem that builds quietly and surfaces late.

Aggregate productivity tends to follow a J-curve: organizations first go through a period of adoption costs and friction before benefits materialize in the overall data. Those expecting immediate returns may stop investing just before those returns arrive.

The competitive landscape among models has shifted

The performance of leading models from Anthropic, Google, OpenAI, and xAI is now close enough that it no longer constitutes a measurable competitive advantage. Competitive pressure has shifted to cost, reliability, and real-world usefulness in operational contexts.

“Jagged intelligence” describes a structural characteristic of current systems: the same model that wins a gold medal at the International Mathematical Olympiad fails to read an analog clock correctly more than half the time. Understanding where a system is reliable — and where it isn’t — has become a management competency before it’s a technical one.

The report introduces the “Centaur Evaluations” framework: measuring the combined performance of a human and an AI system working together, rather than AI performance in isolation. It’s a metric closer to real-world utility in business contexts.

Agents are advancing, security is holding back the leap

AI agents have made a significant jump: accuracy on computer-use benchmarks went from 12% to 66% in a single year. Organizational interest is high. Yet 62% of executives cite security and risk management as the primary obstacle to full-scale deployment. The gap between experimentation and real scale remains wide.

Two structural vulnerabilities worth bringing to the boardroom

TSMC dependency. Virtually every frontier AI chip is fabricated by a single foundry in Taiwan. The entire global AI value chain is concentrated on a single geographic point. Added to this is the dependency on High-Bandwidth Memory (HBM), dominated by just three producers: SK Hynix, Samsung, and Micron.Training data is running out. High-quality publicly available text for training models is projected to reach exhaustion between 2026 and 2032. Organizations that own curated proprietary data — and know how to leverage it — are building a structural competitive advantage that will be hard to replicate. The proprietary data licensing market is already moving in this direction.

The governance picture

Formal internal AI oversight structures grew 17% in 2025. The main obstacles to implementation remain: knowledge and training gaps (59%), budget constraints (48%), and regulatory uncertainty (41%). Documented AI-related incidents rose from 233 in 2024 to 362 in 2025.

On the regulatory front, the EU activated the first provisions of the AI Act in 2025. The United States has instead moved toward deregulation to foster innovation. Sovereign supercomputing clusters in Europe and Central Asia grew from 3 to 44 between 2018 and 2025: governments view control over AI infrastructure as a matter of national security.

Neodata analyzes the data that matters to help organizations navigate AI integration with method and awareness.